An original analysis of Companies House data covering 13 hospitality SIC codes reveals that 233,732 new businesses were registered between January 2023 and February 2026, compared to 173,175 dissolutions. That is a net gain of over 60,000 businesses. Every single sub-sector of UK hospitality recorded positive net growth. The industry is churning, not dying.

What the Headlines Say

Open any newspaper or news site and the story about UK hospitality writes itself. “One pub closing every day” (The Guardian, January 2026). “382 net closures in Q4 2025” (CGA/AlixPartners, via The Independent). “2,076 hospitality venues could close in 2026” (UKHospitality). “3,353 hospitality insolvencies in the year to December 2025” (The Drinks Business, citing Begbies Traynor).

Those numbers are real. The closures are real. The pressure on operators from rising business rates, higher employer NICs, and energy costs is real. Nobody is disputing that.

But there is a number that never appears in any of those headlines: how many new hospitality businesses opened in the same period.

We went to Companies House and counted.

233,732 new hospitality companies registered. 173,175 dissolved. Net result: +60,557 more businesses than when we started counting. 36 out of 38 months recorded net positive growth.

The Number Nobody Reports

We pulled data from the Companies House Advanced Search API for all 13 SIC codes that cover UK hospitality, from hotels and holiday parks through to takeaways, pubs, and event caterers. The data covers every month from January 2023 to February 2026: 38 consecutive months of incorporation and dissolution figures.

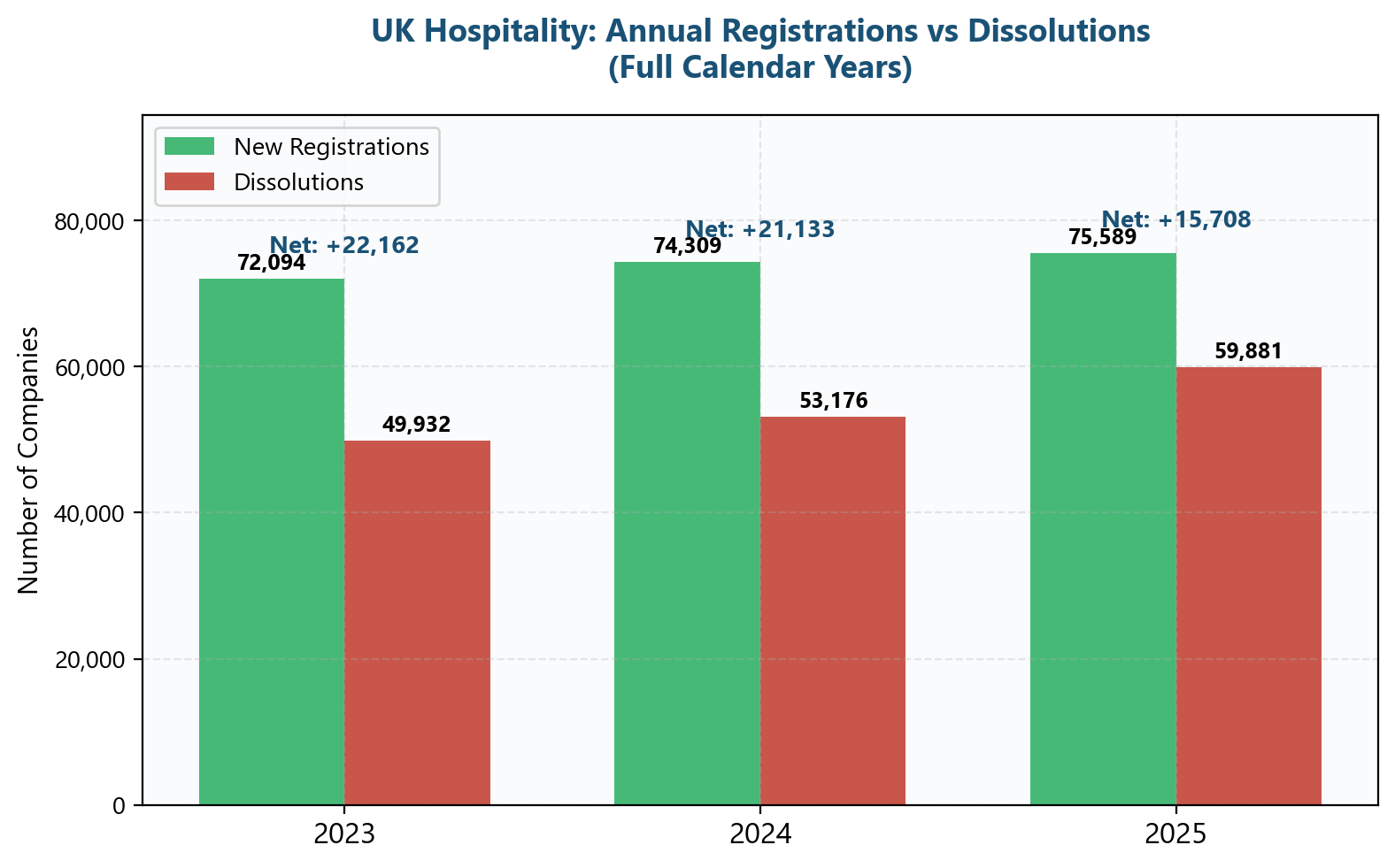

The annual totals tell a clear story:

| Year | New Registrations | Dissolutions | Net Change | Ratio |

| 2023 | 72,094 | 49,932 | +22,162 | 1.44x |

| 2024 | 74,309 | 53,176 | +21,133 | 1.40x |

| 2025 | 75,589 | 59,881 | +15,708 | 1.26x |

| 2026 (Jan-Feb) | 11,740 | 10,186 | +1,554 | 1.15x |

In 2023, for every hospitality business that dissolved, 1.44 new ones registered. In 2024 the ratio was 1.40x. Even in 2025, when the cost pressures were at their most intense and the headlines were at their bleakest, the ratio stayed above 1.26x. New registrations still outpaced dissolutions every single full calendar year in the dataset.

The two months that did go negative were December 2024 and December 2025. Both Decembers. That is not a sector in decline. That is normal seasonal behaviour: fewer people register new companies over Christmas, and dissolution paperwork that has been working through the system all year gets finalised in Q4.

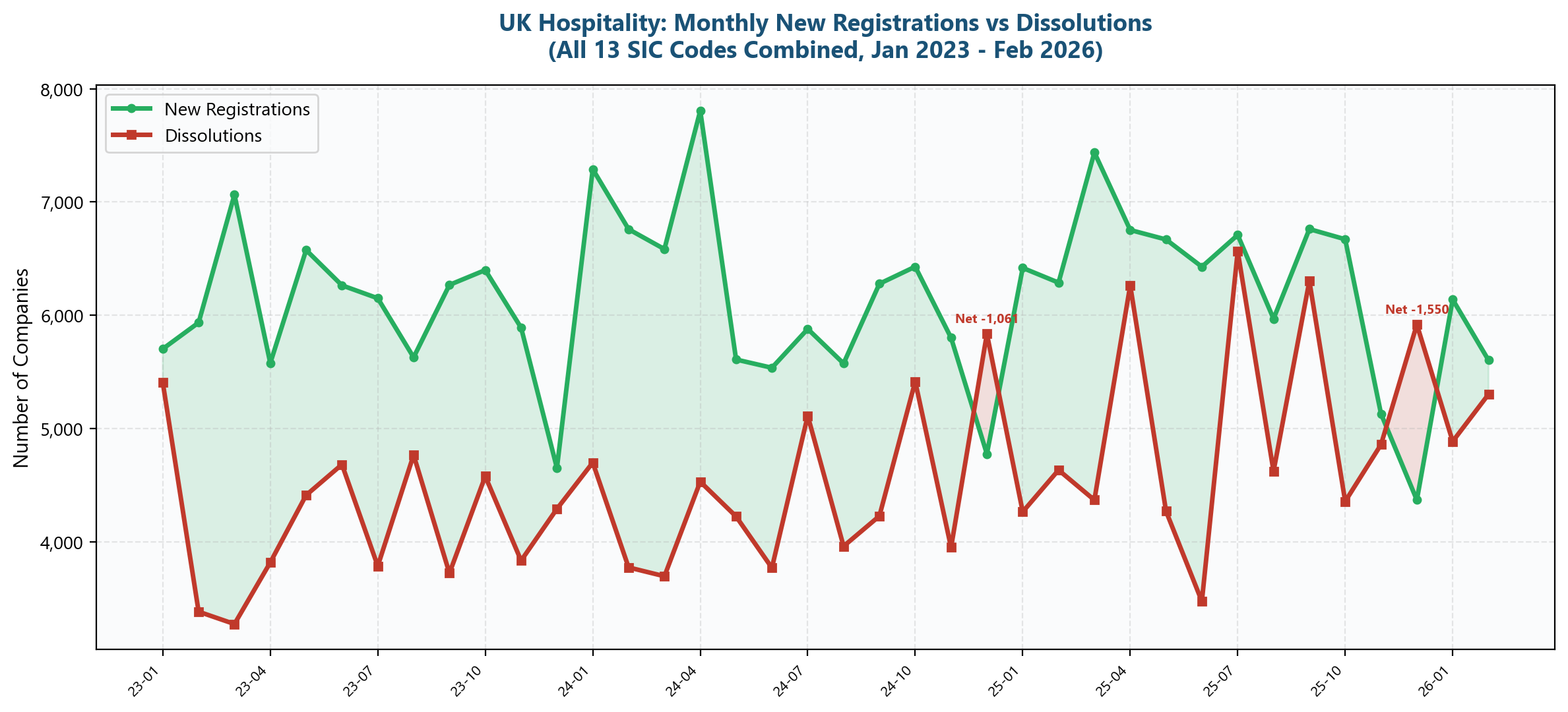

36 Out of 38 Months: Net Positive Growth

The monthly chart makes the pattern hard to argue with. New registrations (green) sit above dissolutions (red) in almost every month. The green shaded area between the two lines is the net gain: new businesses entering the market faster than old ones leave.

March is consistently the strongest month for new registrations. Operators who spend January and February planning their new venture get it officially registered in March, ready for the spring and summer trading season. January is the second-strongest month, likely driven by New Year business launches.

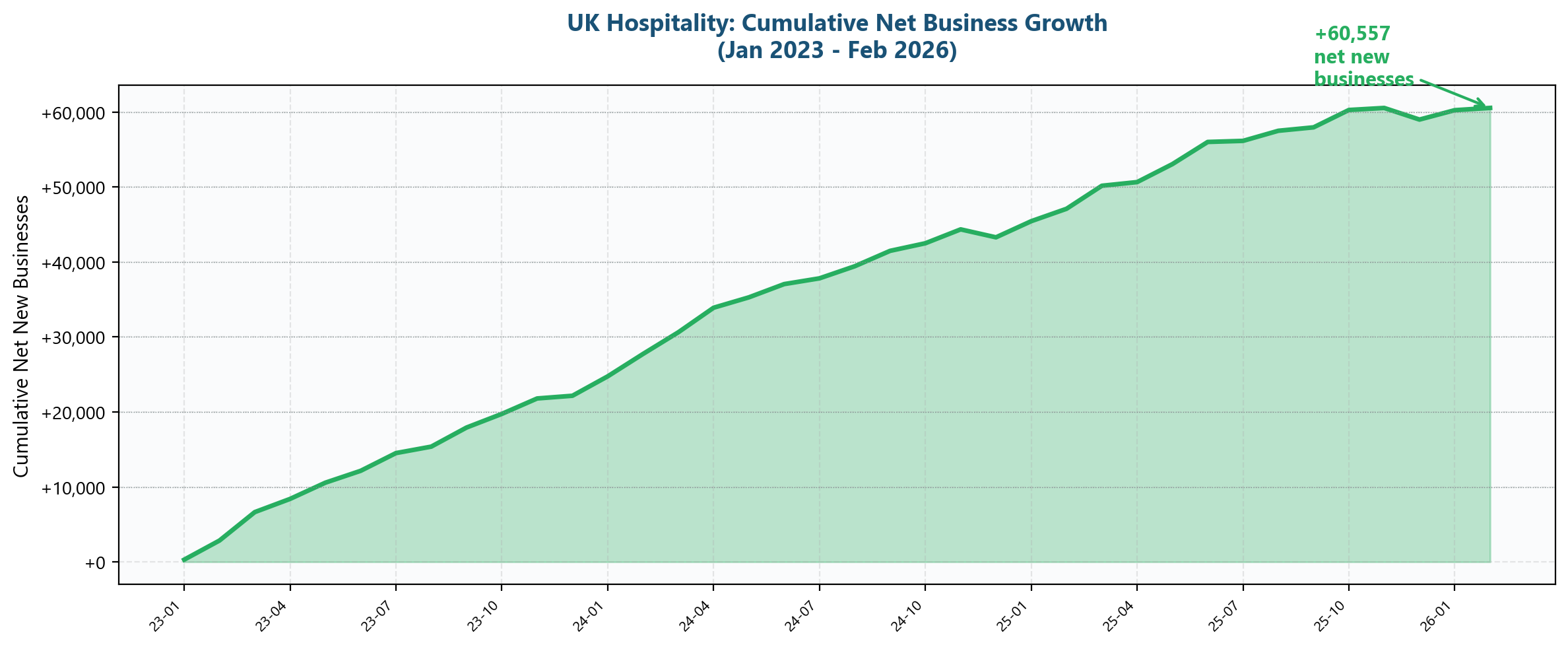

The cumulative picture is even more striking. The running total of net new businesses has climbed steadily from zero in January 2023 to over +60,000 by February 2026. There is no plateau. There is no downturn. The line keeps going up.

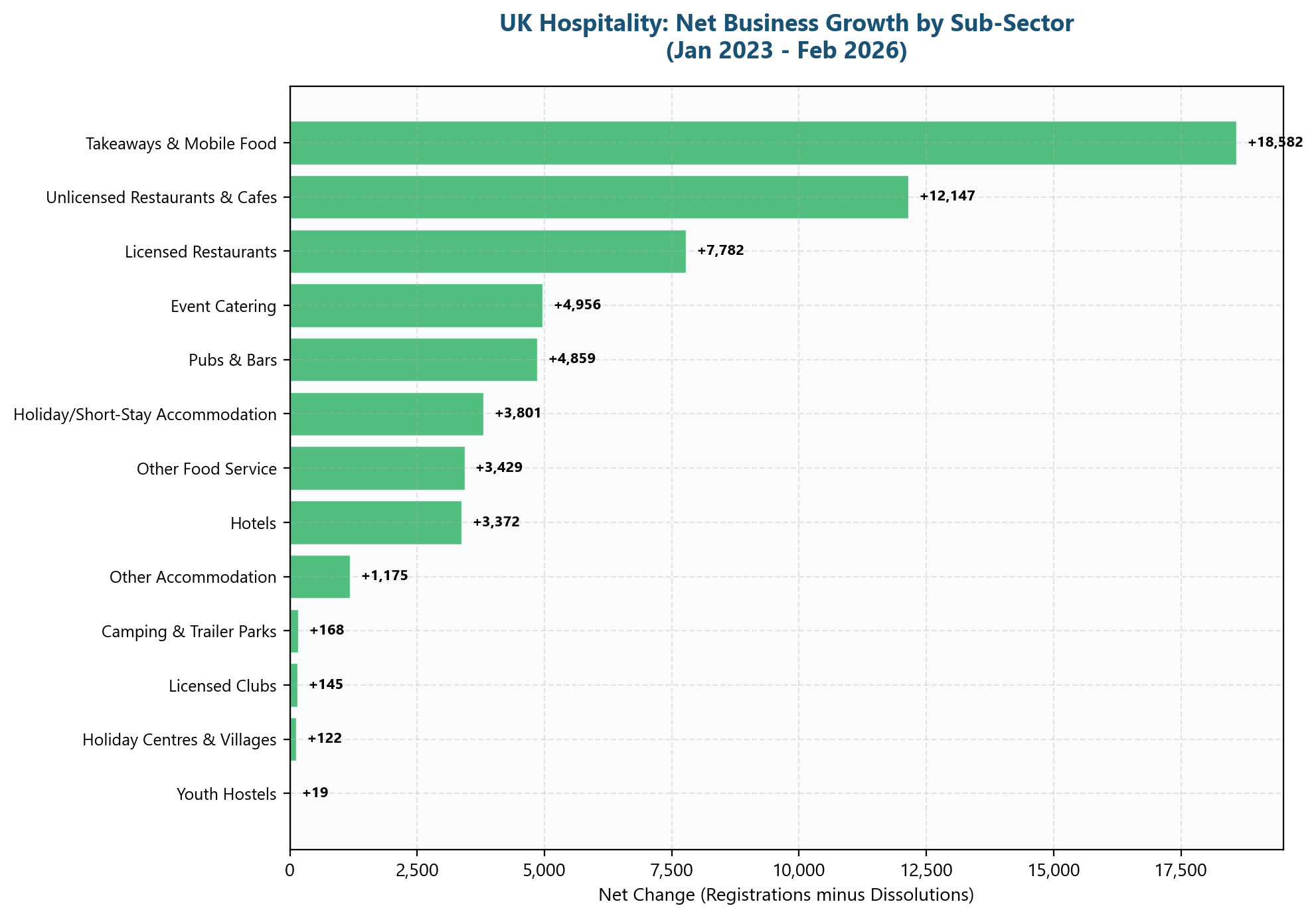

All 13 Sub-Sectors Recorded Net Growth

This is the finding that surprised us the most. It is not just takeaways or cafes driving the numbers. Every single one of the 13 hospitality SIC codes tracked by Companies House recorded a net positive change over the period.

| Sub-Sector | New Registrations | Dissolutions | Net Change | Ratio |

| Takeaways & Mobile Food | 71,028 | 52,446 | +18,582 | 1.35x |

| Unlicensed Restaurants & Cafes | 35,064 | 22,917 | +12,147 | 1.53x |

| Licensed Restaurants | 33,457 | 25,675 | +7,782 | 1.30x |

| Event Catering | 23,215 | 18,259 | +4,956 | 1.27x |

| Pubs & Bars | 22,983 | 18,124 | +4,859 | 1.27x |

| Holiday/Short-Stay Accommodation | 8,205 | 4,404 | +3,801 | 1.86x |

| Other Food Service | 21,660 | 18,231 | +3,429 | 1.19x |

| Hotels | 9,997 | 6,625 | +3,372 | 1.51x |

| Other Accommodation | 4,913 | 3,738 | +1,175 | 1.31x |

| Camping & Trailer Parks | 1,134 | 966 | +168 | 1.17x |

| Licensed Clubs | 1,358 | 1,213 | +145 | 1.12x |

| Holiday Centres & Villages | 514 | 392 | +122 | 1.31x |

| Youth Hostels | 204 | 185 | +19 | 1.10x |

A few things stand out:

- Takeaways dominate: Takeaways lead on volume with +18,582 net new businesses. We covered this in detail in our previous article, The UK Takeaway Boom

- Cafes are resilient: Unlicensed cafes and restaurants have the second-highest net growth (+12,147) and the strongest ratio of the main food service categories at 1.53x. New cafes tend to stick around

- Pubs are still net positive: Yes, pubs are under pressure. The 1.27x ratio is the lowest among the food service categories. But even pubs recorded +4,859 net new businesses. For every pub that dissolved, 1.27 new pub companies were registered. The pub is transforming, not disappearing

- Staycations are booming: Holiday and short-stay accommodation has the highest ratio of any category at 1.86x. For every holiday let company that closed, nearly two new ones registered. The staycation trend and Airbnb effect are still creating new businesses

So Why Does Everyone Think Hospitality Is Dying?

Because the data that gets reported only tells one side of the story.

The mainstream hospitality data that makes the news comes from sources like CGA (now part of NIQ), which tracks licensed premises. UKHospitality tracks its membership. The Insolvency Service publishes insolvency numbers. All of these focus on what is closing, failing, or shrinking.

Nobody systematically reports the other side: how many new companies are registering.

There are a few reasons for this blind spot:

- Closures are more newsworthy

A well-known restaurant closing down or a pub that has been open for 150 years shutting its doors is a story people care about. Fifty new takeaway companies registering at Companies House in a random Wednesday is not.

- Aggregate data hides the churn

CGA data from The Drinks Business shows that in 2024, 4,078 licensed venues closed and 4,085 new ones opened, a near-perfect replacement. But the headline was about the closures, not the openings. The churn itself is the story, but it never gets framed that way.

- New companies are invisible until they become established

A dissolved pub had customers, staff, a physical presence. A newly registered takeaway company might not start trading for months. By the time it opens, nobody connects it to the registration data.

- Trade bodies have an incentive to emphasise the negative

UKHospitality, the BBPA, and CAMRA all advocate for policy changes: lower business rates, reduced duty, employer NIC relief. The most effective way to make that case is to lead with the pain. That is legitimate lobbying, but it does create a skewed public narrative.

Churn, Not Decline: What the Data Actually Shows

The word that best describes UK hospitality right now is not “decline”. It is “churn”.

Churn means businesses are closing and opening at high rates simultaneously. Old formats that no longer work, such as traditional wet-led pubs, are being replaced by formats that do, like food-led pubs, takeaways, dark kitchens, and specialist cafes. Established businesses that cannot absorb rising costs are making way for newer, leaner operators who have built their cost base around today’s reality.

The ONS Business Demography data for 2024 backs this up. It recorded 30,000 business births and 26,000 business deaths in the Accommodation and Food Services sector, with a birth rate of 14.9% and a death rate of 12.9%. Three-quarters of those new businesses had two or more employees. These are real operations, not dormant shell companies.

This churn has three important implications:

- For operators: If you are an existing operator struggling with costs, you are not alone. But the businesses replacing you are not ghost companies. They are real entrepreneurs who have looked at the same cost environment and decided the opportunity is still worth it

- For suppliers: The constant flow of new business registrations creates continuous demand for commercial kitchen equipment. Every new takeaway, cafe, or restaurant needs fryers, ovens, refrigeration, and prep tables from day one

- For policymakers: Blanket support for “saving” hospitality misses the point if the sector is replacing itself. The real question is whether the churn rate is healthy and whether the new entrants are viable in the long term

What This Means for Equipment Demand

233,732 new hospitality company registrations in 38 months. That works out at roughly 6,150 new companies every month, or about 200 every day.

Not all of them will start trading. Some will be holding companies, some will change direction before they open. But even if half of them fit out a commercial kitchen, that represents continuous, year-round demand for catering equipment at a scale that most people do not appreciate.

The profile of these new operators matters too. They are entering the market at a time of high costs and tight margins. They are overwhelmingly small businesses (the ONS data shows 75% have two or more employees, meaning they are micro-businesses, not large chains). They are price-sensitive from day one.

That is exactly the market that B-Grade and competitively priced new equipment serves. A startup takeaway operator looking at a £25,000 equipment bill can cut that by 30-50% with B-Grade, saving £7,500 to £12,500 without compromising on quality, performance, or compliance.

You can browse the full B-Grade range at h2products.co.uk/product-category/b-grade-catering-equipment, or view new equipment at h2products.co.uk/product-category/brand-new.

Frequently Asked Questions

Is the UK hospitality industry growing or declining?

It depends on what you measure. The number of established licensed premises has declined since 2020, and insolvencies remain historically high. But Companies House data shows that new company registrations consistently outpace dissolutions. Between January 2023 and February 2026, there were 233,732 new hospitality registrations against 173,175 dissolutions, a net gain of over 60,000 businesses. The sector is churning rapidly, with old formats being replaced by new ones.

How many new hospitality businesses open each year in the UK?

According to our analysis of Companies House data, approximately 72,000 to 75,000 new hospitality companies are registered each year (covering all 13 SIC codes in Divisions 55 and 56). The ONS Business Demography report for 2024 recorded 30,000 business births in the Accommodation and Food Services sector.

How many hospitality businesses close each year in the UK?

Companies House data shows between 50,000 and 60,000 hospitality company dissolutions per year. The Insolvency Service recorded 3,353 hospitality insolvencies in the 12 months to December 2025 (Begbies Traynor). CGA/AlixPartners data shows 4,078 licensed venue closures during 2024.

Which hospitality sub-sector is growing the fastest?

By volume, takeaways and mobile food stands (SIC 56103) lead with +18,582 net new businesses over three years. By ratio, holiday and short-stay accommodation has the strongest growth at 1.86 new businesses for every dissolution. Unlicensed restaurants and cafes have the best ratio among food service categories at 1.53x.

Are pubs really closing at a rate of one per day?

The BBPA estimated 378 pub closures across England, Wales, and Scotland in 2025. The total number of pubs in England and Wales fell from 38,989 to 38,623 between December 2024 and December 2025. But Companies House data shows 22,983 new pub and bar companies registered over the same three-year period against 18,124 dissolutions, a net gain of +4,859. The pub sector is transforming: traditional wet-led pubs are closing, but food-led pubs, micropubs, and taprooms are opening.

What is B-Grade catering equipment?

B-Grade equipment is brand-new, unused commercial kitchen equipment that has minor cosmetic imperfections or damaged packaging. It comes with full manufacturer warranties and meets all current UK hygiene and safety standards. B-Grade pricing typically offers savings of 30 to 50% off the retail price, making it an attractive option for startup operators.

Data Sources and Methodology

| Source | Data Used | Access |

| Companies House API | Advanced Search API: incorporations and dissolutions for all 13 hospitality SIC codes (Divisions 55 and 56), Jan 2023 to Feb 2026 | Free API (API key required) |

| ONS Business Demography | Business births and deaths by sector, 2024 | Free download from ons.gov.uk |

| CGA / AlixPartners | Licensed premise closures and openings 2024-2025, via trade press | Third-party reports |

| Insolvency Service | Hospitality insolvency figures cited via Begbies Traynor | gov.uk monthly statistics |

| UKHospitality | Venue closure projections for 2026 | Trade body reporting |

| BBPA | Pub closure figures 2025 | Trade body reporting |

All Companies House data was collected and analysed in March 2026. The dataset covers 13 SIC codes across Divisions 55 (Accommodation) and 56 (Food and beverage service activities). Monthly data was collected for each SIC code via the Advanced Search API. Dissolution data uses the “dissolved” company status filter with date ranges.

References

Mainstream sources cited in this article:

- The Guardian. “One pub closing per day in England and Wales.” January 2026.

- The Independent. “382 net closures in Q4 2025.” Citing CGA/AlixPartners Market Recovery Monitor.

- “2,076 hospitality venues could close in 2026.” Sector modelling, February 2026.

- The Drinks Business. “3,353 hospitality insolvencies in year to December 2025.” Citing Begbies Traynor.

- CGA/AlixPartners. Market Recovery Monitor: 4,078 venue closures and 4,085 openings in 2024.

- “378 pub closures in 2025.” Annual pub count survey.

- “1,086 pubs shut between January and October 2025.” Pub closure tracking.

- “Business demography, UK: 2024.” 30,000 births, 26,000 deaths in Accommodation and Food Services.

- “UK Hotels Forecast 2026.” RevPAR growth forecasts for London and UK regions.

- Mordor Intelligence. UK hospitality industry projected at USD 63.80 billion in 2026.